Aerospace Gear Market Outlook 2026–2030: Growth Drivers, Demand Forecast & Key Trends

Executive Summary

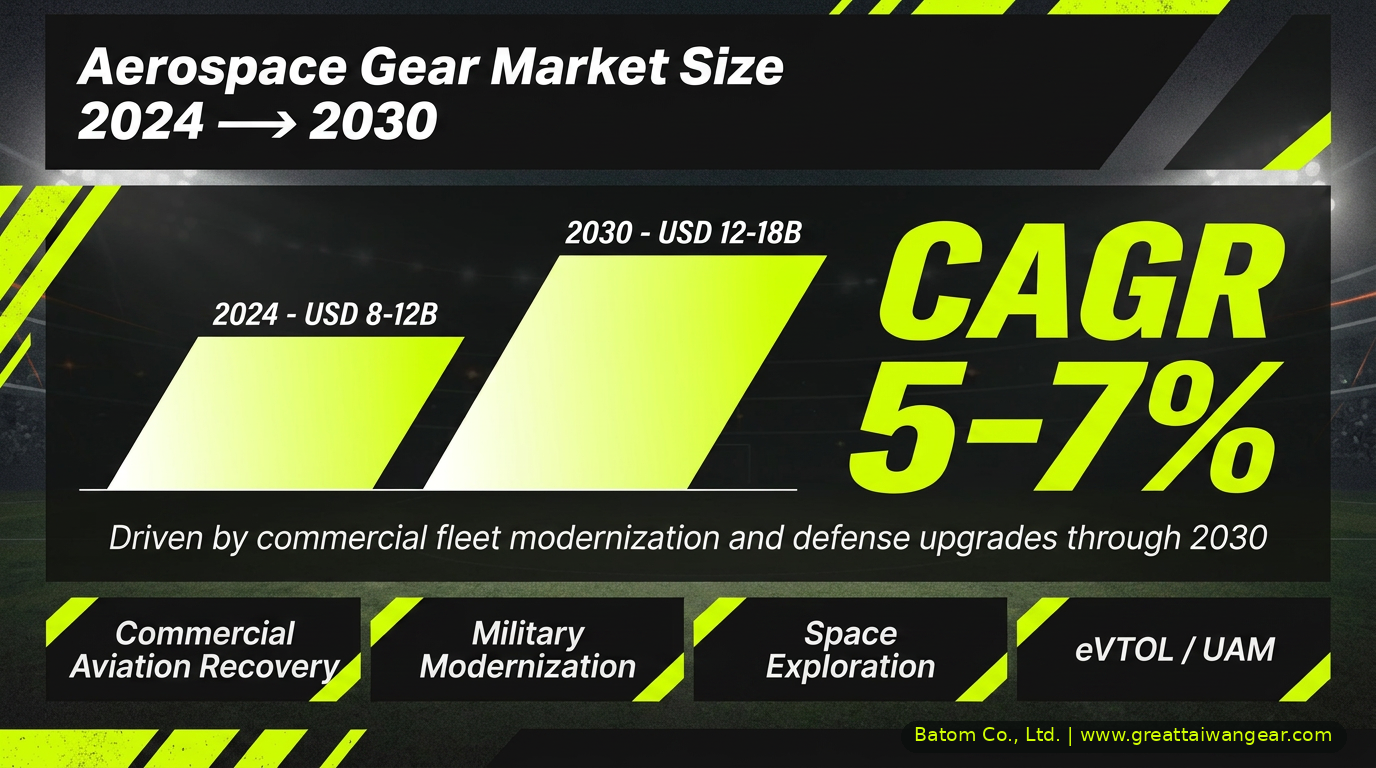

The global aerospace gear market stands at the threshold of significant expansion, driven by commercial aviation recovery, military modernization, emerging aerospace technologies, and increased space exploration activities. The market is projected to grow from USD 8–12 billion in 2024 to reach USD 12–18 billion by 2030, representing a compound annual growth rate (CAGR) of 5–7%. This comprehensive analysis examines market dynamics, demand forecasts across key segments, technological innovations, and strategic opportunities for manufacturers worldwide.

Market Overview and Size Projection

Current Market Status

The global aerospace gear market was valued at approximately USD 8–12 billion in 2024. The market has recovered strongly from pandemic-related disruptions and continues to expand driven by:

- Recovery of commercial aviation operations globally

- Increased defense spending in key regions

- Technological advancement in aerospace applications

- Emergence of new aircraft categories and mission profiles

Growth Projections 2026–2030

Based on comprehensive market analysis, the aerospace gear market is projected to expand at a CAGR of 5–7% through 2030, reaching a total addressable market of USD 12–18 billion. This growth trajectory is supported by multiple converging trends and market segments.

Growth Drivers and Market Catalysts

1. Commercial Aviation Fleet Expansion

Global commercial aviation has entered a sustainable growth phase with consistent increase in aircraft deliveries. The expansion of commercial air transport is driven by:

- Rising Air Travel Demand: Strong passenger traffic growth is expected in emerging markets

- Fleet Modernization: Airlines replacing older aircraft with fuel-efficient models (Boeing 737 MAX, Airbus A320neo, A350)

- New Routes and Capacity: Expansion of air routes in Asia-Pacific and African markets

- Aftermarket Services: Growing maintenance, repair, and overhaul (MRO) activities supporting aging fleets

Commercial aerospace gears are essential components in engine gearboxes, auxiliary power units (APU), and landing gear systems. The increasing number of aircraft deliveries directly translates to higher demand for aerospace-grade gears.

2. Military Modernization and Defense Spending

Global defense budgets are increasing with regional powers investing heavily in fighter aircraft modernization, transport aircraft upgrades, and helicopter fleet expansion. Key drivers include:

- Geopolitical Tensions: Regional security concerns driving military equipment investments

- Technology Upgrades: Retrofitting existing aircraft with advanced systems

- New Platform Development: Development of 6th-generation combat systems and continued modernization of 5th-generation fleets such as the F-35 remain key priorities, with growing demand for flight control actuation, landing gear systems, mission-critical transmission components, and high-reliability actuator gears.

- Unmanned Systems: Growth in military unmanned aerial vehicles (UAVs) and advanced drone systems

Military gears command premium pricing due to stringent reliability, durability, and performance specifications, making this segment highly profitable for suppliers.

3. Electric Vertical Takeoff and Landing (eVTOL) and Urban Air Mobility (UAM)

The eVTOL and UAM sector represents one of the most dynamic growth opportunities for aerospace gears. Key developments include:

- Regulatory Framework: Certification pathways established in multiple jurisdictions

- Investment Growth: Over USD 12 billion invested in eVTOL companies globally through 2024

- Fleet Deployment Plans: Multiple operators targeting commercial service launch in 2025–2028, subject to evolving regulatory certifications.

- Technology Readiness: Advanced prototype testing demonstrating commercial viability

eVTOL aircraft require specialized, lightweight, high-efficiency gear systems optimized for electric propulsion. This market segment is projected to grow at 20–25% annually through 2030, representing a transformative opportunity for innovative suppliers.

4. Space Exploration and Commercial Satellite Industry

The commercial space sector continues rapid expansion with:

- Satellite Launch Acceleration: Thousands of internet constellation satellites deployed

- Commercial Space Stations: Development of orbital platforms and space tourism vehicles

- Deep Space Exploration: NASA lunar program and interplanetary missions

- Launch Vehicle Reusability: Reusable rocket technology enabling cost reduction

Space applications demand highly specialized gears with extreme reliability and performance characteristics, commanding premium valuations and supporting advanced R&D capabilities.

5. Fuel Efficiency and Environmental Regulations

Increasingly stringent environmental and fuel efficiency regulations drive development of:

- Advanced Engine Technologies: Geared turbofan engines with improved efficiency

- Lighter Materials: Weight reduction through advanced composites and alloys

- Hybrid-Electric Propulsion: Development of hybrid and fully electric propulsion systems

- Noise Reduction Technologies: Gear design innovation for noise reduction

Demand Forecast by Segment

Commercial Aviation (Market Share 45%, USD 5.4–8.1B by 2030)

Current Status: Largest market segment with established supply chains and mature production techniques.

Growth Projections: 4–5% CAGR through 2030

Demand Drivers:

- Global commercial aircraft fleet size projected to reach over 40,000 units by 2030, alongside steady annual delivery growth.

- Fleet maintenance and aftermarket operations supporting aging aircraft

- Engine gearbox systems in modern turbofan engines

- Auxiliary power units (APU) for ground operations

Key Applications:

- Main engine gearbox assemblies

- Auxiliary power unit (APU) gearboxes

- Landing gear transmission systems

- High-lift device actuators and landing gear actuation systems

Strategic Importance: High-volume segment with standardized components and established relationships with major OEMs (Boeing, Airbus) and Tier-1 suppliers.

Military Aviation (Market Share 25%, USD 3.0–4.5B by 2030)

Current Status: Premium segment with specialized requirements and long development cycles.

Growth Projections: 5–6% CAGR through 2030

Demand Drivers:

- Fighter aircraft modernization programs

- Military transport aircraft acquisition

- Helicopter fleet expansion and upgrades

- Next-generation platform development

Key Applications:

- Combat aircraft transmission systems

- Helicopter main rotor and tail rotor gearboxes

- Military transport aircraft systems

- Advanced rotorcraft platforms

Strategic Importance: High-margin segment with extended product lifecycles, comprehensive testing requirements, and secure long-term contracts. Premium pricing reflects stringent military specifications.

Rotorcraft and Helicopter Operations (Market Share 15%, USD 1.8–2.7B by 2030)

Current Status: Specialized segment with diverse applications from civilian to military operations.

Growth Projections: 5–7% CAGR through 2030

Demand Drivers:

- Helicopter fleet expansion for emergency medical services (EMS)

- Offshore operations and petroleum services

- Utility and transport helicopter programs

- Urban air mobility development

Key Applications:

- Main gearbox assemblies

- Tail rotor drive systems

- Intermediate gearboxes

- Auxiliary power systems

Strategic Importance: Specialized applications requiring customized solutions and close integration with helicopter manufacturers and operators.

Space and Satellite (Market Share 10%, USD 1.2–1.8B by 2030)

Current Status: Fastest-growing segment driven by commercial space explosion.

Growth Projections: 12–15% CAGR through 2030

Demand Drivers:

- Commercial satellite constellation launches

- Space station payload deployment

- Lunar lander and rover missions

- In-space manufacturing and resource utilization

Key Applications:

- Satellite platform mechanisms and actuators

- Orbital docking systems

- Lunar vehicle drives

- Space telescope mechanisms

Strategic Importance: Highest-specification segment demanding exceptional reliability, extreme temperature performance through solid-film lubrication, and fully maintenance-free operation over multi-year missions.

Emerging Technologies and eVTOL (Market Share 5%, USD 0.6–0.9B by 2030)

Current Status: Nascent but rapidly developing segment with transformative potential.

Growth Projections: 20–25% CAGR through 2030

Demand Drivers:

- eVTOL aircraft development and certification

- Urban air mobility infrastructure development

- Hybrid-electric propulsion system development

- Advanced battery and electric motor technologies

Key Applications:

- Electric motor drives and transmission systems

- Advanced reduction gearboxes for electric propulsion

- Hybrid power management systems

- Digital control and monitoring systems

Strategic Importance: Innovation-intensive segment requiring close collaboration with emerging OEMs, technology partners, and regulatory bodies. Early participants will establish market leadership positions.

Technology Trends and Innovation Roadmap

1. Additive Manufacturing and 3D Printing

Additive manufacturing is revolutionizing aerospace gear design and production:

Current Applications:

- Prototype development and rapid iteration

- Complex internal geometry optimization

- Low-volume specialized components

- Repair and replacement parts

Expected Advancement by 2030:

- Growing adoption of additive manufacturing in non-critical or specialized aerospace gears, with increasing integration into hybrid processes.

Benefits:

- Weight optimization potential through complex internal geometries and the consolidation of multi-part assemblies into fewer, integrated components.

- Optimized power transmission characteristics

- Reduced manufacturing lead times

- Enhanced design flexibility for customized solutions

2. Advanced Materials and Alloy Development

Material science advancement continues driving performance improvements:

Advanced Gear Steels:

- Advanced secondary-hardening steels such as M50NiL, paired with controlled heat treatment for high-temperature gear applications

- Carburizing and nitriding processes optimized for elevated service temperatures

- Surface engineering and coatings for enhanced wear resistance and durability

Lightweight Structural Innovations:

- Advanced topology-optimized lightweight alloy structures using aerospace-grade metals to reduce mass while maintaining stiffness, durability, and certification readiness.

- Advanced resin systems for elevated temperature performance

- Composite bearing surfaces and stress-relieving geometries

Novel Steel Developments:

- Ultra-clean VIM/VAR forged steels with exceptional fatigue resistance and stringent inclusion control.

- Nano-engineered steel with enhanced fatigue resistance

- Corrosion-resistant coatings for extended service life

3. Digital Twin and Industry 4.0 Integration

Digital transformation of manufacturing processes:

Smart Manufacturing Features:

- Real-time process monitoring and quality control

- Predictive maintenance scheduling based on component condition

- Virtual testing and simulation before physical production

- Interconnected supply chain visibility

Benefits:

- 10–15% improvement in production efficiency

- Significant enhancement in first-pass yield and process consistency.

- Extended component service life through optimized maintenance

- Rapid response to production issues and adjustments

4. Predictive Maintenance and Condition-Based Monitoring

Transition from scheduled to condition-based maintenance:

IoT and AI Integration:

- Embedded sensors for real-time vibration and temperature monitoring

- Machine learning algorithms for failure prediction

- Integration of advanced telemetry to monitor gear mesh frequencies, vibration signatures, temperature trends, and lubricant debris in real time.

- Cloud-based asset management systems

Operational Benefits:

- Enhanced predictive capabilities supporting improved reliability and maintenance planning for critical aerospace components.

- Extended time-on-wing for aircraft engines

- Reduced spare parts inventory requirements

- Improved operator safety and reliability

5. Noise and Vibration Control

Advanced gear design and manufacturing techniques:

Noise Reduction Technologies:

- Precision tooth profile modifications

- Optimized gear mesh geometry

- Damping material integration

- Advanced surface finishing techniques

Performance Targets:

- Targeting up to 3–5 dB noise reduction compared to conventional designs.

- Enhanced passenger comfort in commercial aviation

- Reduced operational noise in urban air mobility applications

- Compliance with increasingly stringent environmental regulations

Regional Market Analysis

North America (Market Share 40%, USD 4.8–7.2B by 2030)

Market Characteristics:

- Established aerospace industrial base with Boeing, Airbus suppliers, and domestic manufacturers

- Advanced technology infrastructure and R&D capabilities

- Stringent regulatory environment and certification requirements

- Integrated supply chain across manufacturing and assembly

Growth Drivers:

- Commercial aircraft production recovery

- Military modernization spending

- eVTOL industry development and ecosystem

Projected Growth: 4–5% CAGR

Key Players: Established OEMs, Tier-1 suppliers, and specialized manufacturers

Europe (Market Share 30%, USD 3.6–5.4B by 2030)

Market Characteristics:

- Airbus and integrated European supply chain

- Strong engineering and manufacturing capabilities

- Advanced technology centers and research institutions

- Emphasis on sustainability and environmental performance

Growth Drivers:

- Airbus aircraft production expansion

- Defense spending and military modernization

- Advanced manufacturing technology adoption

Projected Growth: 5–6% CAGR

Key Players: Airbus suppliers, component manufacturers, and research organizations

Asia-Pacific (Market Share 20%, USD 2.4–3.6B by 2030)

Market Characteristics:

- Fastest-growing region with expanding aerospace ecosystem

- Cost-competitive manufacturing base

- Rising domestic commercial aviation demand

- Government aerospace industry development programs

Growth Drivers:

- Rapid growth in commercial aviation and fleet expansion

- Emerging aerospace manufacturers and high-precision manufacturing hubs, with Taiwan playing a growing role in the regional supply chain.

- Rising military spending in region

- eVTOL and urban air mobility development

- Satellite and space industry expansion

Projected Growth: 6–8% CAGR

Key Opportunities for Asian Manufacturers:

- Cost-competitive production for global supply chains

- Regional final assembly and integration centers

- Specialized component manufacturing

- Emerging market supply for regional operators

- Technology partnership and joint venture opportunities

Other Regions (Middle East, Latin America, Africa) (Market Share 10%, USD 1.2–1.8B by 2030)

Market Characteristics:

- Emerging aerospace sectors with growth potential

- Maintenance and repair services for aging fleets

- Growing aviation infrastructure development

Projected Growth: 4–5% CAGR

Supply Chain Analysis and Challenges

Current Supply Chain Structure

The aerospace gear supply chain comprises multiple tiers:

- Tier-1 Suppliers: Major component suppliers to OEMs and final assemblers

- Tier-2 and Tier-3: Specialized manufacturers and material suppliers

- Support Services: Maintenance, repair, and logistics providers

Within this structure, specialist Tier-2 and Tier-3 manufacturers play a decisive role in delivering the high-precision processes that aerospace transmission components demand. Batom Co., Ltd. operates in this space, providing advanced gear manufacturing and finishing capabilities aligned with aerospace quality requirements:

Core Manufacturing Capabilities:

- Gear Grinding and Combo Grinding for Class 3–5 (AGMA) precision tolerances

- Profile, lead, and pitch correction on a single setup for reduced cumulative error

- Tight surface-finish control supporting fatigue life and noise reduction

Commissioned Inspection & Finishing Services:

- Magnetic particle inspection

- Grinding burn inspection

- Particle cleanliness inspection

- Full dimension inspection of various gears

- Abrasive Flow Machining (AFM)

- Abrasive Flow Polishing

- Abrasive Flow Deburring

This combination of high-precision processing and traceable inspection services positions Batom as a reliable partner for OEMs and Tier-1 suppliers seeking aerospace-grade quality with disciplined process control.

Key Challenges

1. Raw Material Constraints:

- Limited availability of high-temperature superalloys

- Price volatility in specialized steel and titanium markets

- Environmental and compliance requirements for material sourcing

2. Production Capacity:

- Current capacity approaching saturation during demand peaks

- Capital-intensive manufacturing infrastructure

- Skilled workforce availability limitations

3. Certification and Compliance:

- Extended aerospace product qualification and certification processes often span multiple years for critical transmission components.

- Complex documentation and traceability requirements

- Environmental and sustainability regulations

- Robust defense supply chain cybersecurity practices, including CMMC-aligned information handling, help protect CUI, design data, and manufacturing records across the aerospace supply chain.

4. Geopolitical and Supply Chain Risks:

- Global tensions affecting supplier diversification

- Trade policy uncertainty and tariff impacts

- Recent global supply chain disruptions and ongoing geopolitical shifts highlighting structural fragilities.

- Critical material sourcing dependencies

Opportunities for Asian Manufacturers

1. Cost Competitiveness:

- Highly competitive cost structures

- Efficient operational management

- Scalable production capacity

2. Capacity Expansion Potential:

- Available infrastructure investment capacity

- Growing skilled manufacturing workforce

- Government support for aerospace industry development

3. Technology Advancement:

- Access to international technology partnerships

- Capacity to implement advanced manufacturing techniques

- Investment in R&D and innovation capabilities

4. Market Diversification:

- Supply to diverse OEMs and Tier-1 suppliers

- Regional and emerging market focus

- Aftermarket and maintenance services

5. Supply Chain Integration:

- Regional manufacturing and assembly consolidation

- Vertical integration of key components

- Logistics and distribution hub development

- Long-term forecasting, vendor-managed inventory (VMI), and strategic buffer stocking are essential to mitigate long material lead times.

Strategic Imperatives for OEMs & Tier-1 Integrators

For OEMs and Tier-1 integrators evaluating the next generation of aerospace gear suppliers, the following procurement criteria help separate proven aerospace-grade partners from general precision manufacturers. Each criterion reflects an attribute that mature aerospace programs typically require from their qualified vendor list.

Quality Systems and Certification Status

- Require suppliers to maintain active AS9100 certification and Nadcap accreditation for the relevant special processes, as baseline indicators of process discipline, traceability, and supply chain reliability.

- Verify that suppliers operate documented First Article Inspection (FAI) procedures aligned with AS9102, with independent test and validation capabilities for dimensional, metallurgical, and surface-integrity verification.

- Confirm long-standing relationships with recognized certification bodies and a demonstrable history of successful re-audits and merit status renewals.

- Look for evidence of structured continuous improvement programs (e.g. SPC, 8D, internal audit cadence) rather than ad-hoc corrective action.

Engineering and Design Support Capability

- Prioritize suppliers offering early-stage Design for Manufacturability (DFM) consultation, so material selection, tooth geometry, and heat-treatment strategy are optimized before tooling investment.

- Assess in-house R&D depth across advanced materials, additive manufacturing pilots, and digital process technologies — capabilities that indicate readiness for next-generation programs.

- Validate that the supplier collaborates with technology partners, research institutions, or material specialists rather than relying solely on customer-supplied specifications.

- Review whether the supplier maintains an internal innovation roadmap aligned with eVTOL, space, and geared turbofan trends, signalling forward technical alignment with OEM programs.

Program Partnership and Supply Chain Integration

- Seek suppliers willing to operate as long-cycle program partners with OEMs and Tier-1 integrators, not transactional job-shops.

- Confirm the supplier can support localized manufacturing or regional integration scenarios while adhering strictly to applicable export control and compliance frameworks (ITAR/EAR, regional dual-use regulations).

- Evaluate the supplier's participation in industry working groups or emerging standards committees as an indicator of credibility and forward visibility.

- Confirm interoperability with complementary Tier-2 and Tier-3 manufacturers, so the supplier integrates smoothly into a multi-source aerospace supply chain.

Market Focus and Product Portfolio Fit

- Favor suppliers with specialized product lines or process capabilities targeted at defined aerospace segments (engine accessory gearboxes, rotorcraft transmissions, actuator gear trains, space mechanisms) rather than generic precision machining.

- Look for value-added services such as NVH optimization, application engineering consultation, and strict configuration management — signs that the supplier understands aerospace program economics.

- Assess brand reputation and reference programs: OEM letters of approval, Tier-1 long-term agreements, and verifiable program participation are stronger signals than marketing claims.

- Evaluate the maturity of the supplier's customer relationship management, including dedicated program managers, account engineering support, and structured escalation paths.

Operational Discipline and Delivery Reliability

- Partner with suppliers demonstrating robust lean manufacturing, continuous improvement, and automated production capabilities, so the program benefits from consistent cycle times, predictable cost structures, and disciplined process control.

- Assess supply chain resilience: dual-sourced raw materials, qualified secondary heat-treatment partners, and contingency capacity for AOG or surge-demand scenarios.

- Require evidence of long-term forecasting collaboration, vendor-managed inventory (VMI), and strategic buffer-stocking arrangements to mitigate the long material lead times typical of aerospace alloys.

- Verify structured workforce training programs, sustainability commitments, and environmental management systems, all of which reduce program risk over multi-year contract horizons.

Frequently Asked Questions

Q1: What is the primary driver of aerospace gear market growth?

A: Commercial aviation recovery combined with military modernization spending, emerging aerospace technologies (eVTOL/UAM), and space exploration activities represent the primary growth catalysts. The market is supported by multiple converging demand vectors rather than dependence on a single segment.

Q2: Which market segment offers the highest growth potential?

A: The space and satellite segment (12–15% CAGR) and emerging eVTOL/UAM technologies (20–25% CAGR) offer the highest growth rates. However, commercial aviation remains the largest market by volume, representing 45% of total demand.

Q3: What competitive advantages do Asian manufacturers possess?

A: Highly competitive cost structures, scalable capacity, technology advancement capability, and a growing aerospace ecosystem represent key competitive advantages. Regional proximity to emerging markets also provides strategic benefits.

Q4: How will digital technologies and Industry 4.0 impact the market?

A: Digital technologies enable predictive maintenance, production optimization, and enhanced quality control, supporting meaningful gains in efficiency, first-pass yield, and reliability. Adoption of Industry 4.0 practices will become increasingly important for competitive positioning.

Q5: What certification and compliance requirements should manufacturers address?

A: Aerospace quality management certification (AS9100), material traceability systems, and rigorous process controls are foundational. Environmental compliance, including REACH considerations for chemical processes, along with strict adherence to applicable export control and supply chain traceability requirements, are critical. Manufacturers should establish comprehensive quality systems and long-term certification planning to ensure market access and customer confidence.

Conclusion

The aerospace gear market stands at the beginning of a transformative growth period (2026–2030), driven by commercial aviation expansion, military modernization, emerging aerospace technologies, and space exploration activities. The projected market growth to USD 12–18 billion by 2030 represents significant opportunity for manufacturers worldwide.

For Asian manufacturers, this represents a strategic inflection point. By investing in quality excellence, technological innovation, and strategic partnerships, Asian suppliers can capture market share in this expanding market while establishing themselves as preferred partners for global aerospace OEMs and Tier-1 suppliers. The manufacturers who successfully combine cost competitiveness with quality excellence and technological advancement will position themselves as industry leaders in the next decade.

As a premier manufacturer based in Taiwan, Batom combines Asian manufacturing cost-efficiencies with rigorous aerospace quality standards. We welcome opportunities to support global OEM and Tier-1 partners seeking reliable, high-precision gear solutions.